EP249 - Holiday shipping data from ShipBob

Casey Armstrong (@CaseyA) is CMO at ShipBob, a third party logistics provider that offers e-commerce fulfillment for thousands of brands. They are able to see the carrier shipping performance for all those clients and provide aggregate data that gives us insight into holiday shipping performance, also known as #shipageddon.

Episode 249 of the Jason & Scot show was recorded live on Monday, December 7th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP248 - Cyber 5 with Salesforce's Rob Garf

Rob Garf (@retailrobgarf) the VP of Strategy and Insights, Retail and Consumer goods at Salesforce. Rob also earned a 10/10 from @ratemyskyperoom which makes me extremely jealous.

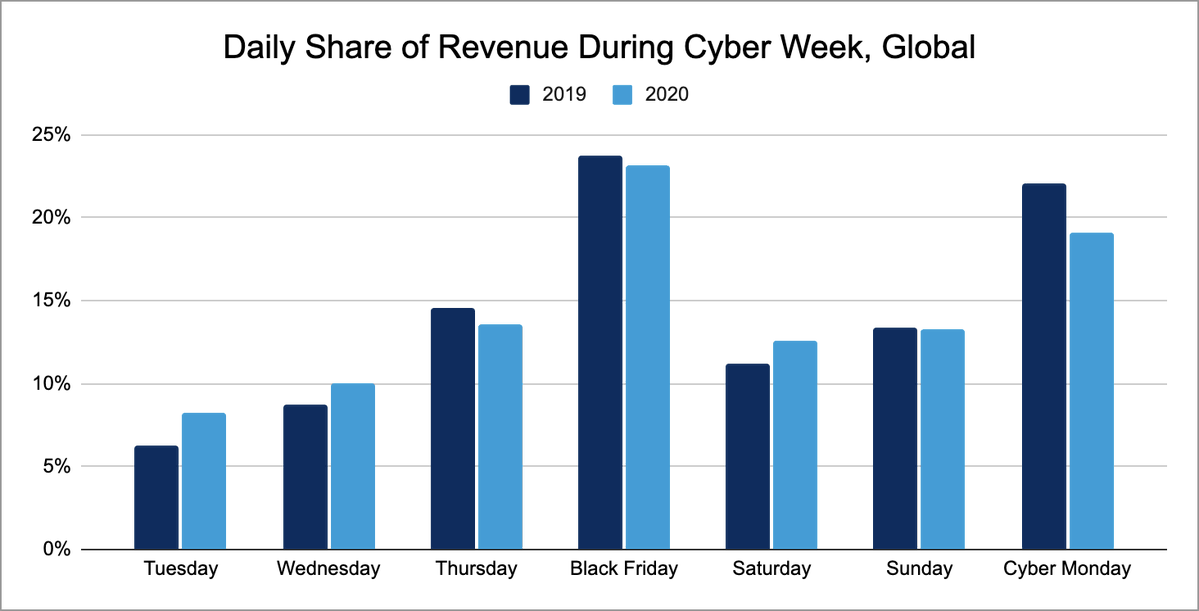

Cyber Week online sales unfolded in the pattern we expected after the first three quarters of the year. Digital sales surged an unprecedented 71% in Q2 globally and significantly grew 55% in Q3 globally. We forecast 30% growth for the entire holiday season, November 1 – December 26. For the largest two digital days of the season, specifically, Black Friday came in right on target with 30% growth and Cyber Monday grew at a lower rate of 18% year-over-year (YoY) globally.

- Salesforce Holiday Portal

- Blog Post for Cyber Five

- LinkedIn Livestream from Rob and Jason discussing Cyber Five.

We cover key trends, including changes to holiday behavior due to Covid-19, winners and losers, mobile trends, promotion trends, and omni-channel tactics.

Episode 248 of the Jason & Scot show was recorded live on Tuesday, December 1st, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP247 - Cyber 5 with Adobe

Vivek Pandya is the Senior Digital Insights Manager at Adobe.

Data from Adobe, which uses Adobe Analytics to analyze one trillion visits and 100 million SKUs from 80 of the 100 largest retailers in the U.S., found that consumers spent a whopping $34.4 billion during this year’s Cyber Week, which represents a 20.7 percent year-over-year (YoY) increase. Unsurprisingly, Thanksgiving, Black Friday and Cyber Monday represented the bulk of total spend over the five-day period.

We cover key trends, including changes to holiday behavior due to Covid-19, winners and losers, mobile trends, promotion trends, and omni-channel tactics.

Episode 247 of the Jason & Scot show was recorded live on Tuesday, December 1st, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP246 - Q3 Results

The US Census Bureau published its retail monthly data and quarterly e-commerce data this week. We also saw earnings reports from Target, Walmart, Lowes, Home Depot, Walgreens, and Kohls.

We also discuss Amazon’s entry into pharmacy.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

Episode 246 of the Jason & Scot show was recorded live on Thursday, November 20th 2020.

EP245 - Shipageddon DeepDive

On October 3rd, we published episode 238 and coined the term “Shipageddon.” We were talking about the likely e-commerce peak we expected from the holiday, on top of the e-commerce peak we were already seeing do to Covid-19, and we felt like retailers were likely to run into shipping capacity issues. The term (and concept) have gained a lot of traction, being featured print in the NY Times Brace for Holiday ‘Shipageddon’ Forbes, Bloomberg, and on the Today Show, NBC News, and many others.

In the subsequent 45 days, it’s become clear that we will have a last-mile capacity problem, with all major carriers implementing quotas, turning away new clients, and retailers struggling to entice earlier orders from consumers. Worse, we’re also seeing a lack of freight capacity to restock retailers with limited inventory, and a strong resurgence of Covid-19 threatens to generate even more e-commerce demand.

In this episode, we do a deep dive into the curate state of Shipageddon, the likely impact on holiday shopping, and best practices for brands and retailers to minimize the effect.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 245 of the Jason & Scot show was recorded live on Thursday, Nobember 12th 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP244 - Upfront Ventures Greg Bettinelli

Greg Bettinelli (@gregbettinelli) is a partner at Upfront Ventures. Greg was previously the CMO for LA-based HauteLook, a leading online flash-sale retailer (acquired by Nordstrom). Upfronts portfolio includes ThredUp, Parachute Home, Adore Me, Skylar, Verishop Goat, Happy Returns, Invia Robotics, ChowNow, Verishop and in transportation Fair, Bird, and SureSale.

We discuss DNVBs, Marketplaces, Shipageddon, and much more.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 244 of the Jason & Scot show was recorded live on Thursday, October 28th 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP243 - Amazon Q3 2020 Earnings Recap

In this episode, we break down Amazon’s Q3 2020 earnings (PDF) results.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

Episode 243 of the Jason & Scot show was recorded live on Thursday, October 29th 2020.

EP242 - Salsify Co-Founder and CMO Rob Gonzalez

Rob Gonzales is the Co-Founder and CMO of Salsify an e-commerce enablement SaaS company that has raised over $250m and focuses on helping brands sell online. Rob is also co-founder of the Digital Shelf Institute.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 242 of the Jason & Scot show was recorded live on Wednesday, October 21st 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP241 - Holiday Preview with eMarketer's Andrew Lipsman

Andrew Lipsman (@alipsman) is the Principal Analyst for retail and e-commerce for eMarketer. In this episode, Andrew gives listeners an advanced preview of eMarketer’s holiday forecast, and we do a deep dive into all the factors that will play into this holiday season. This holiday season may have more uncertainty for brands and retailers than any other holiday season in our lifetime, so it’s well worth the listen.

This is an exclusive preview of one of the most anticipated holiday forecasts in the industry.

Key Topics:

- Vectors that influence holiday forecasts

- The forecast

- Shipageddon

- Can retailers pull holiday in early?

- How will the cyber-5 play out

- Returnageddon

- Category winners and losers

- Retail winners and losers

- How to follow the season

eMarketer Holiday 2020 Forecast

- Total retail +0.9% to $1.013 trillion

- Ecommerce +35.8% growth to $190B (+ $50B in ecommerce sales vs. last year)

- Brick-and-mortar -4.7% to $823B

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 241 of the Jason & Scot show was recorded live on Tuesday, October 21, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP240 - Amazon Prime Day Recap

Episode 240 is a recap of Amazon Prime Day 2020, and a review of the US Census Advanced Monthly Retail Sales data for September.

Amazon Prime Day

- Amazon Press Release

- ChannelAdvisor Prime Day

- Salesforce Prime Day Blog

- Two Thirds of Sales During Prime Day Were by Amazon 1P – marketplace Pulse

- Cool PrimeDay Review of 50 e-commerce sites by Forrester research analyst Nicole Murgia

Advanced Retail Sales Data for September

US Census Advanced Monthly Retail Sales for September

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 240 of the Jason & Scot show was recorded live on Friday, October 16th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP239 - Retail Sales Data with US Census Bureau

Paul Bucchioni is Branch Chief and Scott Scheleur is a Supervisory Survey Statistician, both with the Retail Indicator Branch, Economic Indicators Division of the U.S. Census Bureau. In this interview, Paul and Scott walk us through the real sales data products that the US Census publishes and gives us advance about how to interpret the data.

- US Census Retail Data Site

- Twitter Account: @uscensusbureau

- St. Louis Federal Reserve Tool (FRED)

- Google Public Dataset Tool

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 239 of the Jason & Scot show was recorded live on Wednesday, October 7th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP238- Holiday Shipageddon

This holiday season will be a mixed bag for retailers. Health concerns are likely to drive many more consumers online, but can retailers and shippers, who are already experiencing Cyber-Monday levels of e-commerce handle the increased volume?

Scott Silverman (@scottsilverman) of CommerceNext and Ken Cassar (@kcassar) of CassarCo join us to discuss the holiday season, including a CommerceNext survey of 1,000+ consumers, and 60+ digital retail executives to understand how aware they may be of shipping delays, trade-offs they'd be willing to make in order to get free shipping, etc.

- Jason wrote a related article "Holiday 2020: A Mixed Bag For Retailers" in Forbes this week

- The twitter thread that kicked off this discussion

- Lowes locker announcement that Scot mentioned

- Deloitte Holiday Forecast

- Salesforce Holiday Forecast

Don't forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 238 of the Jason & Scot show was recorded live on Thursday, October 1st, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP237 - Always Day One author Alex Kantrowitz

Alex Kantrowitzer (@Kantrowitz) is the author of “Always Day One: How the Tech Titans Plan to Stay on Top Forever.” He is an on-air contributor at CNBC and host of the Big Technology podcast.

In this broad-ranging interview, we discuss the unique management styles at Apple, Google, and Facebook, as well as doing a deep dive into what makes the Amazon culture unique.

Disclosure: links to Amazon are affiliate links.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 237 of the Jason & Scot show was recorded live on Thursday, September 24th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP236 - DNVBs w/ Nate Poulin

Episode 236 is an interview with Nate Poulin aka @digitallynativ about Digitally Native Verticle Brands (DNVBs)..

Upcoming Events

- Digital Day North America Jason & Scot Keynote September 23 8:40-9:25am CT

- Channel Advisor Connect – Jason & Scot October 7th

- Texas A&M Retail Summit Jason October 9th 9:50am CT

- ShopTalk Meetup – Jason October 20-22

Measuring Ecommerce Success Against Fast-Changing Benchmarks.

Topics

Nate Poulin (@digitalnativ) cut his teeth with DNVBs including Bonobos and Outdoor Voices and is currently the Chief Merchant for Monica + Andy. In this episode, we discuss a range of topics around the current state and future of digitally native brands.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 236 of the Jason & Scot show was recorded live on Monday, September 14th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP235 - Amazon Grocery, Walmart+, Holiday Preview

This episode covers the latest Amazon Grocery news, the launch of Walmart+, and our first look at holiday 2020.

Upcoming Events

- CommerceLive – Jason September 15, Noon ET.

Panel: Retailer Search Strategies — What’s Working and What’s Worth It? - Publicis Livestream – Jason & Scot – Thursday, September 17 11:00AM ET

Covid, Holiday 2020, and 2021 - Digital Day North America Jason & Scot Keynote September 23 8:40-9:25am CT

- Channel Advisor Connect – Jason & Scot October 7th

- Texas A&M Retail Summit Jason October 9th 9:50am CT

- ShopTalk Meetup – Jason October 20-22

Measuring Ecommerce Success Against Fast-Changing Benchmarks.

Topics

- Amazon Grocery

- Amazon Fresh – 40K “Non-Whole Foods” grocery concept. Dash Carts (Scan & Go). Microfullfilment? Woodland Hills open, two more free-standing coming to LA, one freestanding coming to Chicago, and a shop in shop with Kohls in LA.

- Amazon Go Grocery – 10K store with just-walk-out technology. A second location opens in Redmond. One coming to Washington DC.

- Wholefoods Digital Only – Darkstore opens in Brooklyn.

- JCP acquired from bankruptcy by Simon Property Group (NYSE: SPG) and Brookfield Property Partners.

- Walmart+ launch (and drone test)

- Holiday Preview

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 235 of the Jason & Scot show was recorded live on Thursday, September 10th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP234 - Listener Questions Live

Episode 234 is a live show featuring live audience questions. Jason & Scot get to interact with listeners live.

Topics

- Jason wrote an article in Forbes, "It’s Time For E-Commerce Marketplace Reform", Scot found it controversial!

- California’s proposed AB 3262, related to product liabilities for marketplaces.

- Amazon's stance on hybrid sellers (both selling wholesale to Amazon, and direct on the marketplace)

- SEO in the Covid era

- What's the next big thing?

- How are retailers addressing digital impulse?

- Why do retailers have separate systems for e-commerce and POS?

Don't forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 234 of the Jason & Scot show was recorded live on Thursday, August 27th, 2020.

http://jasonandscot.com J

oin your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP234 Preview - Listener Question Show Coming Soon

Hi Listeners. We'll be recording a live listener questions podcast on Wednesday August 26th at 7pm PT / 10pm ET.

Send questions in advance to Facebook Or @scotwingo on twitter Zoom details to join the live call: Join from a PC, Mac, iPad, iPhone or Android device: Please click this URL to join.

https://us02web.zoom.us/j/85358703161?pwd=dWdreWdyckR6S1dQcE5nR3JlVWVCQT09 Passcode: 262640

Description: Jason & Scot Show - Listener Questions Or join by phone:

Dial(for higher quality, dial a number based on your current location): US: +1 312 626 6799 or +1 646 558 8656 or +1 301 715 8592 or +1 346 248 7799 or +1 669 900 9128 or +1 253 215 8782 Webinar ID: 853 5870 3161 Passcode: 262640

International numbers available: https://us02web.zoom.us/u/keF1JYoTnM

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP233 - Q2 2020 Retail Earnings and News

US Census Data

- US Census Retail Data website

- Quarterly Retail E-Commerce Sales 2nd Quarter 2020 (PDF)

- St. Louis Federal Reserve Tool (FRED)

- Google Public Dataset Tool

Retail Earnings Updates

- Walmart Comp sales up 9.3% E-commerce up 97%. Transactions down 14%, basket up 27%

- Target SSS up 10.9%, E-Commerce up 195%. 75% e-commerce fulfilled from stores.

- Home Depot SSS up 25%, e-commerce up 100% (60% BOPIS)

- Lowes US Comp sales up 35.1%, E-commerce up 135%

- Kohls – net sales decrease (22.9%)

- TJX – Net sales came in at $6.67b v $9.78 billion YoY ($214M Loss)

2020 Q2 E-Commerce Scoreboard

- Target 195% (same day 300%)

- Etsy 147%

- Lowes 135%

- HomeDepot 100%

- Walmart 97%

- Shopify 97%

- E-commerce overall (US census): 44.5%

- Amazon: 41% overall, 44% US, 3PM grew 53%

- eBay 26%

Other News

- Simon (SPARC) buys Brooks Brothers, (Aéropostale, Forever 21, Lucky Brand)

- JCP suitors – Amazon and Simon

- Shipping sur-charges

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 233 of the Jason & Scot show was recorded live on Wednesday, August 19th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP232 - rue21 CEO John Fleming

John Fleming is the the interim CEO of rue21. John was formerly the global e-commerce CEO for Uniqlo, Chief Merchant at Walmart, and CEO of Walmart.com. He has also served as a board member at Bed Bath & Beyond and Untuckit.

rue21 is an American specialty retailer of women’s casual apparel and accessories with 670 stores that primarily designs and fabricates its’ own products.

In this broad ranging interview, we discuss the challenges and opportunities presented by Covid, Amazon, the direct to consumer model, and the future of retail.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 232 of the Jason & Scot show was recorded live on Thursday, August 13th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP231 - The Forever Transaction author Robbie Kellman Baxter

Robbie Kellman Baxter (@robbiebax) is the best selling author of “The Forever Transaction” and “The Membership Economy.” She has become a well known subject mater expert on subscription and loyalty programs.

In this broad ranging interview, we discuss well known subscription based brands including Dollar Shave Club, Blue Apron, Stichfix, BirchBox, and Netflix. We also cover issues including subscription fatigue, cancelation friction, and Rundles.

You can find out more about Robbie’s consulting work and her podcast at her website.

Disclosure: links to Amazon are affiliate links.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 231 of the Jason & Scot show was recorded live on Thursday, July 30st, 2020.

EP230 - Amazon Q2 2020 Earnings

Amazon Q2 2020 Earnings

- Amazon Q2 2020 Earnings Presentation

- Statement by Jeff Bezos to the U.S. House Committee on the Judiciary

- Revenue at $88.9B vs expectation of $80.7b, a 41% year over year growth.

- Earnings of $10.30 per share vs expectation of $1.90, a 51% year over year growth.

Other Earnings Updates

- Shopify revenue up 97% to $714M (GMV now exceeds eBay)

- eBay revenue up 18% to $2.87B

Don't forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 230 of the Jason & Scot show was recorded live on Thursday, July 31st, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP229 - NRF NXT, Google Commerce, Big Commerce S1

Jason recent events:

- NRF NXT Tuesday, July 21 11:45am–12:30pm EDT “Future of Platforms”

- Forbes Article “Retail’s Great Pivot: How The Pandemic Has Changed Stores’ Criteria For Success From Traffic To Efficiency“

Jason Upcoming Events

- CommerceNext July 29th 4:10 pm EE “Lesson Learned and Thoughts for the Future”

Industry News

- NRF NXT was this week, a digital commerce show from the National Retail Federation (the successor to the Shop.org tradeshow). You can still register for free, and watch all the sessions on demand.

- Google has eliminated commissions for it’s “Buy on Google” feature on google shopping, as well as offering PayPal and Shopify payments.

- Goldman Sachs equity research published: “Global Internet eCommerce’s steepening curve: Raising global forecasts & identifying new winners” July 20,2020. Scot breaks it down.

- eMarketer publishes “US ECOMMERCE BY CATEGORY 2020” July 22, 2020. Jason breaks it down.

- Big Commerce files it’s S-1. (Keep an eye on RetailRoadshow for their roadshow video).

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 229 of the Jason & Scot show was recorded live on Thursday, July 24th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP228 - Bonus Edition: Verizon Panel - The 5G Future of Retail Post-COVID

Scot and Jason hosted a live panel for Verizon, entitled: “The 5G Future of Retail Post-COVID: Challenges and Opportunities.”

The panel featured three guests:

- Christian Guirnalda (@OpenInnovatioNJ), Director, 5G Labs and Innovation Centers, Verizon

- Michele M. Dupré Group Vice President – Vertical Markets/Canada Verizon Enterprise Solutions

- Rob Dravenstott, Chief Technology Officer, Cooler Screens

We covered a variety of topics related to 5Gs potential impact on retail.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 228 of the Jason & Scot show was recorded live on Wednesday, July 8th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

EP227 - Amazon Dash Cart and Other News

Jason recent events:

- Publicis LinkedIn Livestream: Trends & Insights Live “The New Reality of Retail”

- RetailTouchpoints: Retail Strategy 2.0: Separating Urgent From Important

- Brick and Mortar Reborn

- Rob Gonzalez, Peter Crosby, and the Digital Shelf Institute/Salsify “Creative Commerce in the time of covid”

Jason Upcoming Events

- NRF NXT Tuesday, July 21 11:45am–12:30pm EDT “Future of Platforms”

- CommerceNext July 29th 4:10 pm EE “Lesson Learned and Thoughts for the Future”

The Great Debate

Are we in a long-lasting, deep recession, or is at an artificial recession will quickly bounce back from? What should retailers and brands be planning for. Jason and Scot has it out. Who will be right?

Amazon News

- Amazon Dash Cart

- Echo Frames are frames are shipping

- Q4 restrictions on 3pl warehouses

- Prime day in October

- Employee Health Clinics

- Amazon becomes worlds largest advertiser spending $11B a year

- Earning results next week

Other News

- US Census Bureau Data for June is out.

US Real Retail sales were up 5.8% in June, (down from 17.7% in May) but representing a 2nd month of retail recovery. Total retail sales back above Feb levels. (Numbers adj for inflation and including auto). E-commerce up 23% YoY. - Nike leaves Google Shopping

- Google shopping fast shipping tags

- Nike RISE new store concept in Guangzhou, China

- Walmart and Amazon healthcare battle

- Walmart+ coming soon?

- Is digital grocery profitable?

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 227 of the Jason & Scot show was recorded live on Friday, July 17th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.

Blue Cape Ventures founder Hendrik Laubscher

Hendrik Laubscherger (@henlaub) is the CEO and Founder at Blue Cape Ventures. He is a subject matter expert in global marketplaces and cross-border trade. He publishes a very valuable weekly newsletter which you can subscribe to here.

In this broad ranging interview, we discuss global marketplaces, the latest events at Amazon, comparison shopping engines, direct to consumer, cross border trade, venture capital, and the future of commerce.

Don’t forget to like our facebook page, and if you enjoyed this episode please write us a review on itunes.

Episode 226 of the Jason & Scot show was recorded live on Friday, July 9th, 2020.

Join your hosts Jason "Retailgeek" Goldberg, Chief Commerce Strategy Officer at Publicis, and Scot Wingo, CEO of GetSpiffy and Co-Founder of ChannelAdvisor as they discuss the latest news and trends in the world of e-commerce and digital shopper marketing.